- The expectations to see the post-COVID Chinese economy get back on track seem to have been dashed; China’s economic progress remains unstable but with some recent signs of positivity.

- Uncertainty regarding China’s GDP growth remains; however, China is likely to reach or end up very near its 5% GDP target.

- Inflation and industrial underperformance led to substantiated worries about China’s economic vitality, but the most recent data tells a more positive story.

- Draconian issues in the property and financial sectors remain the main challenges as there is still no light at the end of the tunnel.

- China’s youth unemployment is rampant; it has led to a “virtual clash” between the disgruntled youth and the government. The future dynamics of unemployment are no longer accessible – China has decided to stop releasing the figures.

China and Southeast Asia 2023-3: China‘s Bumpy Ride: Economic Turbulence and “Long-Gowned” Youth

Summary

At the end of 2022, hopes were high that China’s economy would recover quickly and, consequently, act as the main catalyst for the growth of the global economy. After three years of stringent zero-COVID restrictions on movement, mandatory mass testing, and interminable lockdowns, the Chinese government decided, relatively unexpectedly, to abandon its zero-COVID policy, which had paralysed manufacturing, suppressed demand and resulted in the most significant slowdown of the country’s economy since the late 1970s. Reactive to the Chinese policy changes, global prices of oil and other commodities increased due to expectations that Chinese demand would skyrocket. However, the reality was much gloomier; kick-starting the world’s second-largest economy and regaining foreign investors’ and entrepreneurs’ trust proved a significant challenge. In addition to this, China’s slowing economic growth is surfacing its long-standing neglected systematic issues. This analytical review focuses on several dimensions: the current state of the Chinese economy and its important indicators, property and banking sectors, and youth unemployment as a significant societal challenge.

The State of the Chinese Economy: Indicators

Economic growth

For the year 2023, the Chinese government has set a growth target of “around 5%” as a sign of more cautious predicting. However, as early as March, China’s Premier Li Qiang noted that reaching this target would not be an easy task. So far, various predictions are all in unison that reaching 5% growth remains a challenge for the Chinese economy.

The beginning of post-COVID 2023 went largely as expected: initial results showed a healthy initial rebound of the economy. However, starting in the second quarter, economic activities began to signal problems. As noted by Wang Tao, a managing director and chief China economist at UBS in Hong Kong, soon afterwards “property recovery faltered, with [housing] sales and starts falling much further, (…) local governments faced financing challenges, tightened fiscal spending, which also constrained growth (…), the industrial sector started to destock and consumption recovery slowed in the second quarter.”

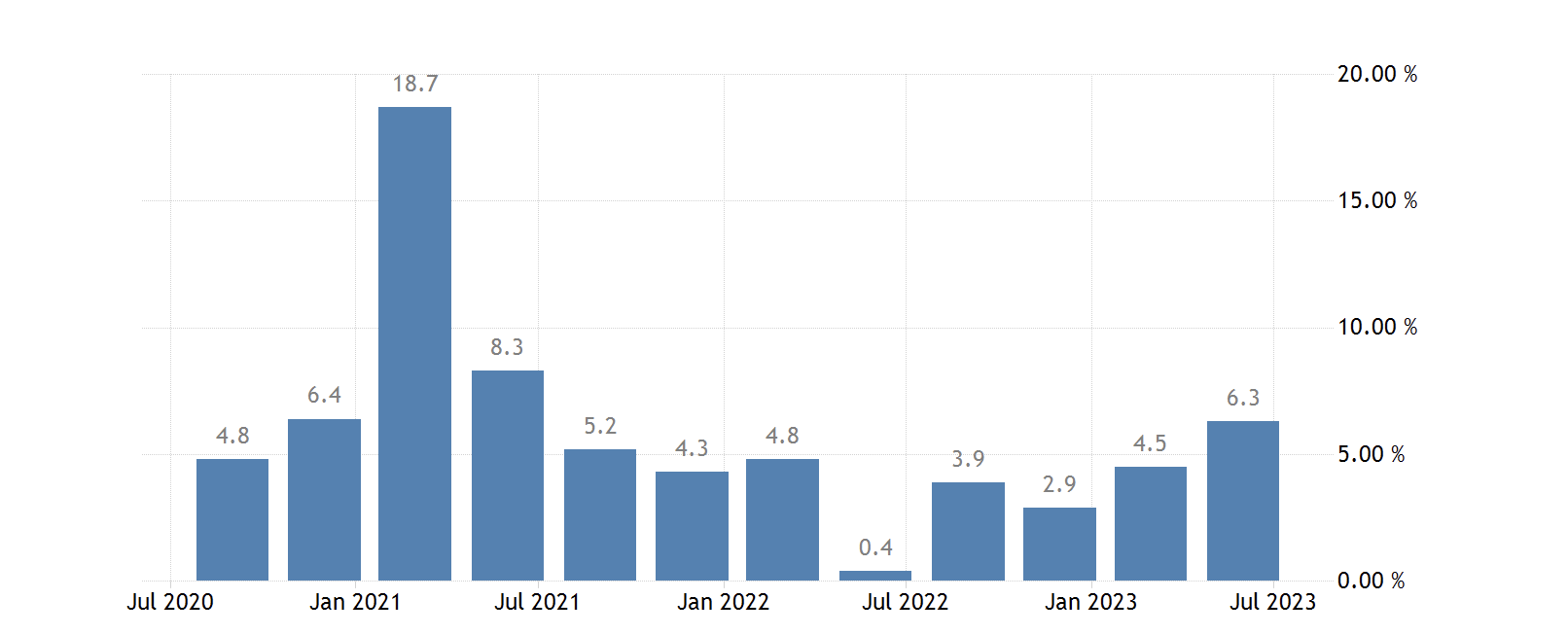

Figure 1: China’s quarterly GDP growth. Source: National Bureau of Statistics of China, Tradingeconomics.com.

However, recent economic data indicates that the economy appears to be stepping out of the sinkhole. In September, despite the remaining challenges that will be discussed below, China’s Premier Li Qiang emphasized that he remains confident in the Chinese economy’s ability to reach the 5% target. However, foreign forecasts are more careful, but still predict that China might just reach the very bottom of its “around 5%” target. In an opinion poll of 76 analysts conducted by Reuters in September, it is predicted that the economy will grow by 5% (in July, this number was 5.5%). This careful but optimistic outlook is a response to the government’s measures to stabilize the economy and, given some economic indicators, some slight positivity is evident.

| Name | 2023 Forecast | 2024 Forecast |

| Barclays | 4.5% | 4% |

| CitiBank | 4.5% | 3% |

| FitchRatings | 4.8% | 4.6% |

| Economist Intelligence Unit | 5.2% | — |

| Moody’s | 5% | 4% |

| Schroders | 4.8% | 4.5% |

| BBVA Research | 4.8% | 4.4% |

Figure 2: The latest forecasts for China’s growth in 2023 and 2024. Source: official websites.

A more positive outlook also emerged from the International Monetary Fund’s press briefing on 28 September. As stated by Julie Kozack, Director of Communications, “what we have seen recently is a slowdown in the economy since the first quarter. However, the very recent data has been a bit more mixed, with some signs of stabilization. We do continue to expect that China will meet its growth target of around 5 per cent in 2023”. This more positive outlook is also closely related to active intervention by the state and the implementation of various measures (see the table below).

| Date | Measures introduced |

| September 1 | Chinese top banks implemented further cuts in lending rates. |

| August 31 | Some borrowing rules were eased to aid real estate buyers, including lower mortgage rates for first-time home buyers and a lower percentage for the down payment required. |

| August 31 | Major Chinese cities announced measures to give out preferential loans for first-home purchases without the verification of their credit records. |

| August 25 | The State Council approved guidelines for planning and construction of affordable housing. |

| August 15 | The People’s Bank of China cut one set of key interest rates. |

| August 2 | The Finance Ministry introduced a set of tax relief measures for small businesses and rural households. |

| July 31 | The State Council introduced measures to boost consumption in the automobile, real estate and services sectors. |

| July 24 | China’s State Planning Commission introduced measures to support private investors in some infrastructure sectors and private projects. |

| July 21 | The State Council introduced guidelines on transforming underdeveloped areas in the major cities – a way to boost property investment. |

| July 19 | The CCP and the State Council announced guidelines to support the private economy with a total of 31 policy measures. |

| July 18 | The Ministry of Commerce announced measures to boost household consumption of goods and services. |

| July 14 | The State Council introduced guidelines aimed at the development of public infrastructure in megacities, aiming to support the economy and prepare for future public health crises. |

Figure 3: Recent measures taken by the government. Source: Reuters.

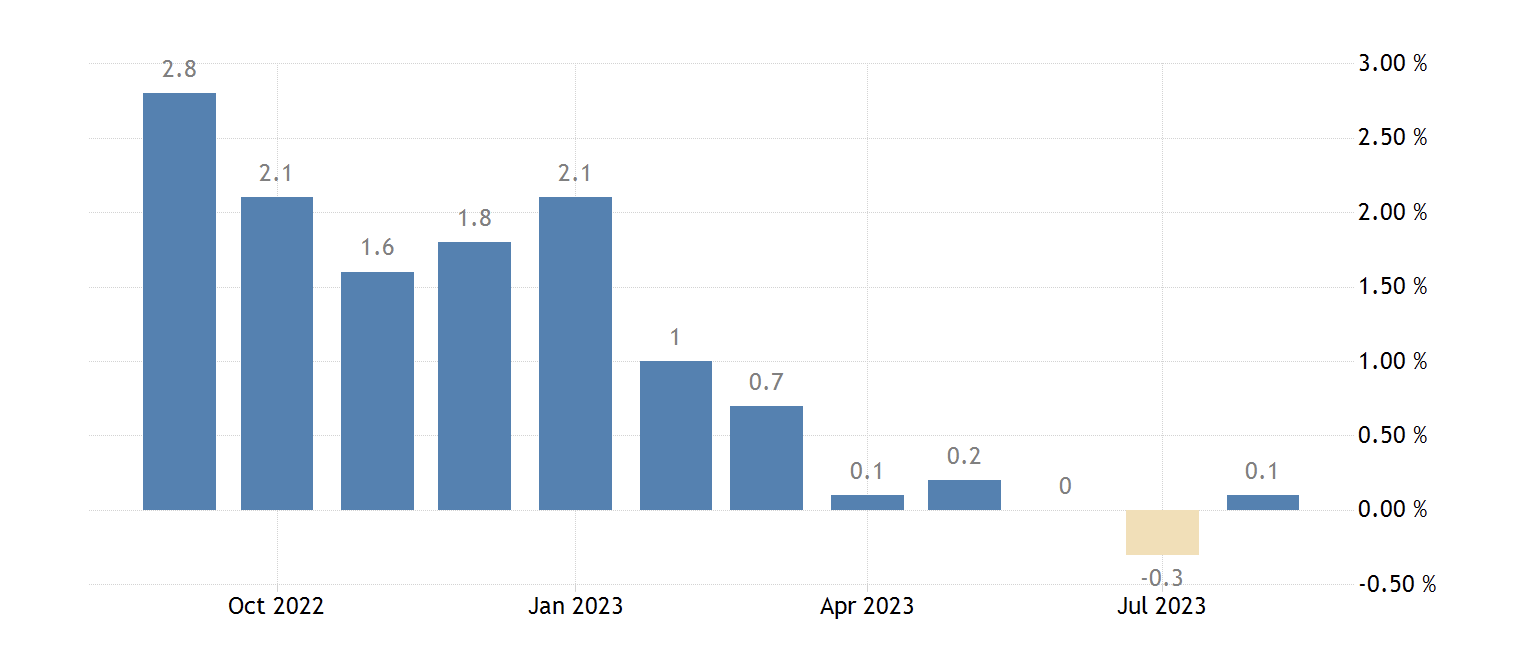

Inflation

In July, China recorded a deflation of -0.3%, leading to concerns that the country might fall into the deflation abyss. However, China’s consumer price level returned to positive numbers in August, which indicates the easing of deflation pressures as a result of signs of stabilization in the Chinese economy. A more positive take on inflation is also reflected in the Western media. However, it is still too early to draw a more accurate picture: China’s consumer prices rose by 0.1% in August 2023, prices in non-food increased by 0.5%, in housing by 0.1%, in healthcare by 1.2%, and in education by 2.5%; however, transport prices fell by 2.1% and food prices fell by 1.7%, with prices of pork falling even further.

Figure 4: Monthly inflation rates. Source: National Bureau of Statistics of China, TradingEconomics.com

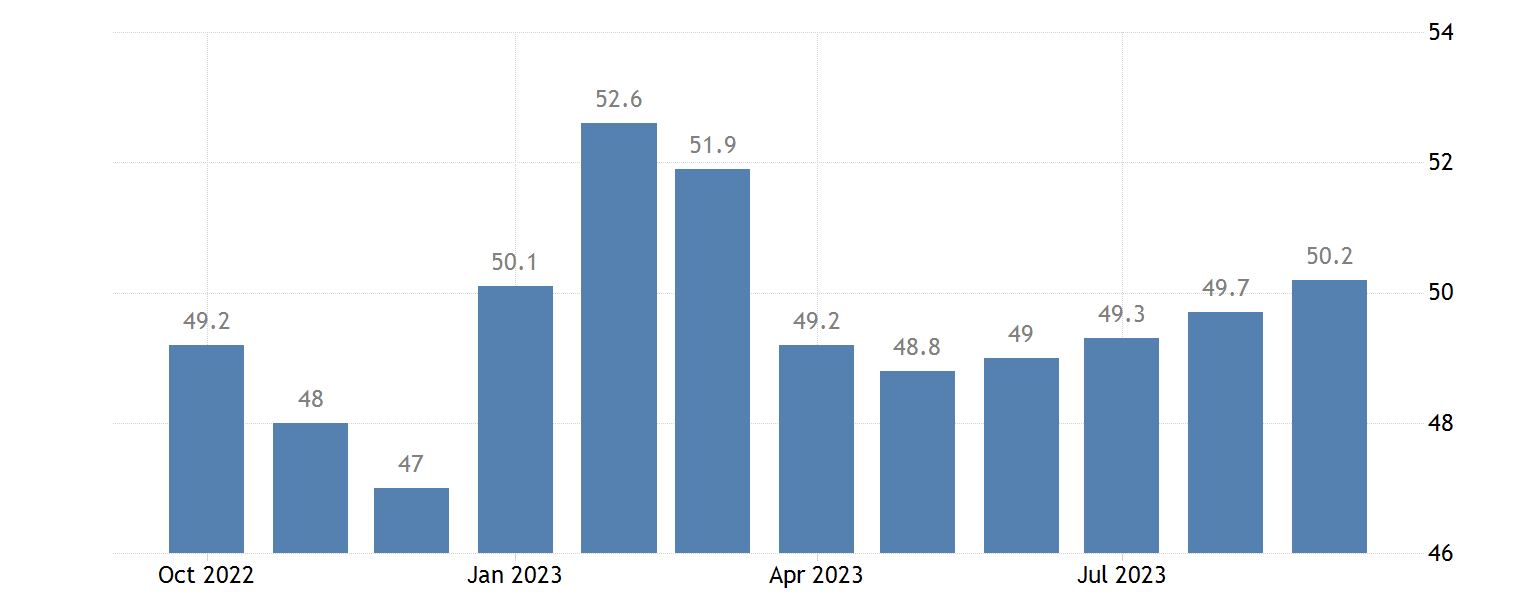

Industrial activity

China’s industrial activity is another important indicator of the health of the manufacturing sector. In this regard, China has also shown a worrying trend: In August, as reported by Reuters, China’s manufacturing activity contracted for a fifth straight month. However, September statistics seem to bring more positivity: for the first time in six months, manufacturing activity signalled expansion.

Figure 5: The official National Bureau of Statistics (NBS) Manufacturing PMI index. Source: Bureau of Statistics of China, Tradingecnomies.com

The official NBS Manufacturing PMI index increased to 50.2 in September 2023 from 49.7 in August, topping market forecasts of 50.0 (above 50 means expansion, below 50 means contraction). September is the first month that saw a shift towards industrial expansion since March, which is related to economic measures taken by the central government. According to the NBS, output continued to increase for the fourth month reaching the fastest pace (52.7), and new orders and buying levels continued to rise for the second month as well (50.5 and 50.7). Foreign sales continued to fall, albeit at a slower pace (47.8). Input costs maintained high growth (59.4) whereas confidence remained relatively high (55.5).

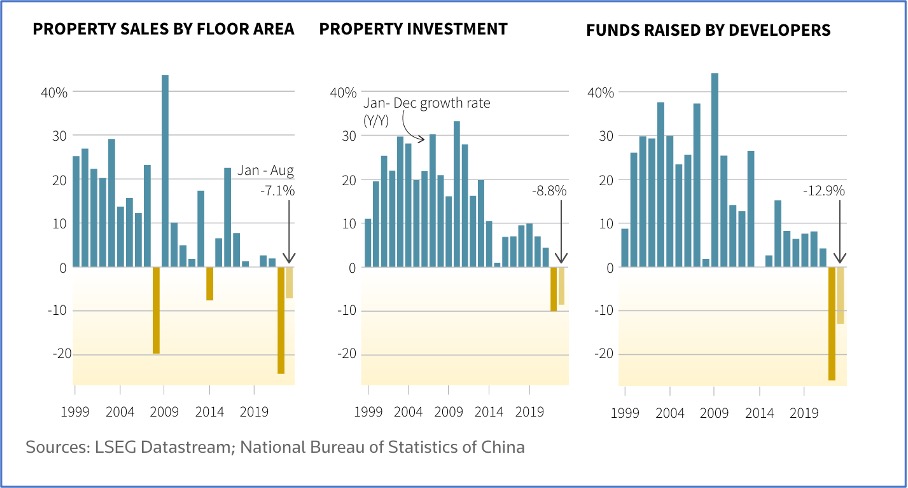

Property sector

Despite growing optimism, China’s property sector remains a draconian challenge for China. The problems, which started as the 2020 Chinese property sector crisis after the introduction of the “three red lines” regulations[1], are nowhere near finished. While the government introduced numerous measures to revive the sector, recent news is rather worrying.

On August 28, upon resumption of trading after a 17-month suspension, Evergrande Group, China’s largest real estate developer, saw its stocks plunge more than 70%. Furthermore, the company’s plan to restructure its debts encountered significant issues: on September 24, Evergrande released a statement noting that it is unable to normalize its operations and proceed to the planned restructuring because its main unit in China, Hengda Real Estate Group, is under investigation. The fate of the company and China’s real estate sector remains muddy.

And the difficulties are complex and deeply rooted. As stated by Grow Investment’s chief economist Hao Hong, “China’s urbanization drive may be drawing to a close — and that could further hurt the already ailing property sector.” The problem kept inflating for years: Chinese urbanization speed, which used to keep up with the fast pace of real estate development, is now reaching its limits. In other words, there might not be enough people to fill the available housing that is built or being built. The inability to maintain a healthy real estate sector is a bigger challenge than it might seem at first sight. Economic vitality and growth are closely connected with the construction sector; any slowdown will have long-term implications. A significant fall in demand and overall expansion will have negative consequences for other sectors such as the financial sector (loans and investments) and the manufacturing sector (home appliances, construction materials etc.). All in all, given China’s decades-long emphasis on the real estate sector as the engine for economic growth, the inability to prevent the collapse of this sector might have devastating consequences.

Figure 6: The State of China’s property sector. Source: LSEG Datastream, National Bureau of Statistics of China.

Banking sector

The eruption of Henan Protests last year revealed systemic problems in the Chinese banking sector, which took a hard hit and significantly reduced society’s confidence in financial institutions. This year, the issues seemed to continue spreading even further. The most recent source of uncertainty is related to the Chinese shadow banking sector. China’s shadow banks are financial institutions that provide investment and loaning services that are not guided by the same regulations as typical banks. This particular sector is closely related to the country’s construction boom as it provided huge loans for project developments. Therefore, problems in the real estate sector are exerting enormous pressure on the shadow banking sector as defaults on payments are beginning to spread.

According to The Economist, shares in Xinhua Trust, a Chinese shadow lender, are being sold at low prices. The report states that company assets including cars were put on an auction as per court order. Small-scale shareholders are even attempting to sell their highly discounted shares on e-commerce platforms. Zhongrong, another major Chinese trust company, recently released a statement providing the reason for missing the payment as due to “external and internal factors”. Zhongzhi Enterprise Group, a major asset management firm, has also revealed to its investors its need to restructure the debt.

Youth Unemployment: “Knowledge alters fate”?

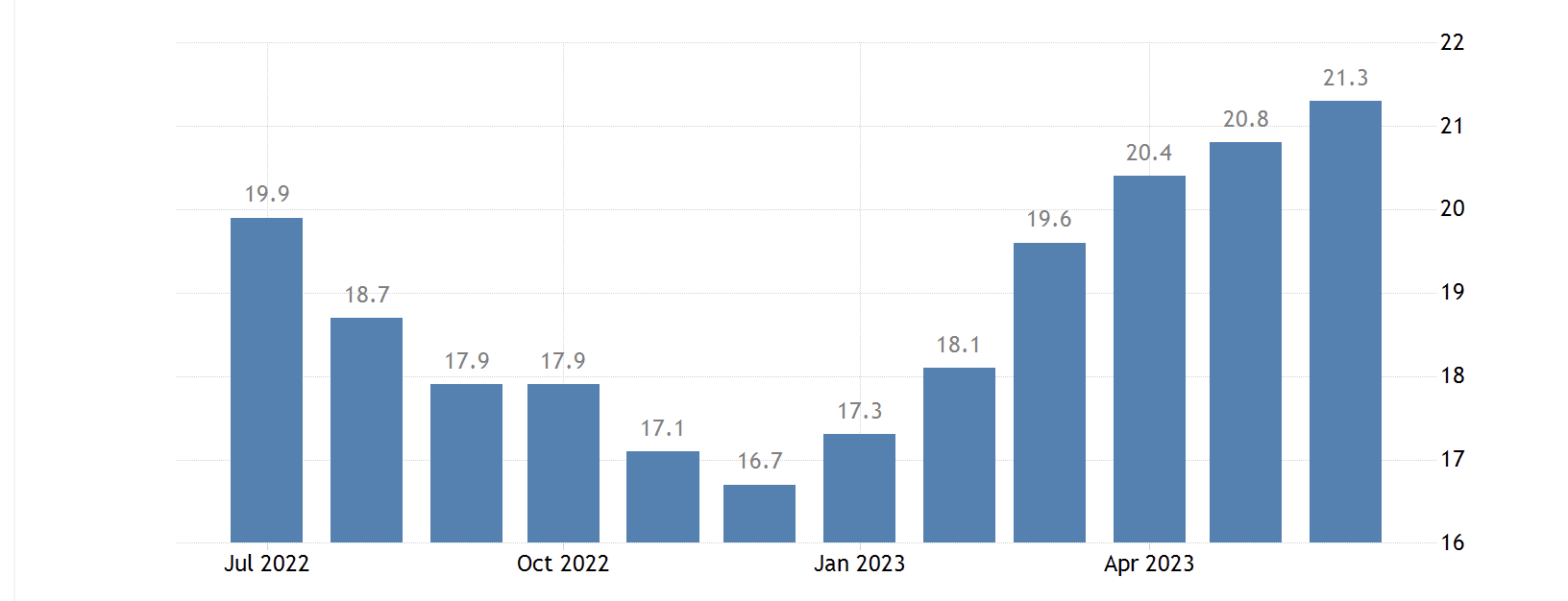

The phrase ”知识改变命运” (“Knowledge alters fate”) used by Xi Jinping in 2018 did not age well. In 2023 China welcomed a record-breaking 11.6 million new graduates. Interestingly, even after lifting COVID restrictions in China, the Chinese unemployment rate not only did not fall but instead climbed even more steeply, in contrast with the experiences in Western countries such as France and Germany.

Figure 7: Chinese youth unemployment rate. Source: National Bureau of Statistics of China, TradingEconomics.com

In 1919, Lu Xun, the founder of modern Chinese literature, wrote the story of “Kong Yiji”. Kong Yiji was a failed scholar who embodied the harsh reality of ‘old’ imperial China and its relentless imperial examination system. His failure in the exams erased any prospects of landing a government position. The story aims to criticize the ‘old’ society in which people could waste entire lives if they fail the examination, and it shows the ‘old’ society’s indifference towards such people. Kong Yiji always wore a long gown and drank while standing – interesting symbolism.[2]

Figure 8: A meme stating: “Youngsters don’t understand Kong Yiji, but when they grow up. they themselves become Kong Yiji’s”

It comes as no surprise that the Kong Yiji story has become popular in recent times, especially among the unemployed youth. Given the significant unemployment rates among the educated youth, Kong Yiji became a popular meme (see Figure 8 above) as a way to criticise the system and the lack of future prospects. However, the deep meaning of Kong Yiji’s story is undoubtedly not in the CCP’s favour. Therefore, Kong Yiji attracted the government’s attention which resulted in an online ‘war of words’. Chinese state media outlet CCTV, whose articles are also echoed in other media outlets, has responded to the Kong Yiji memes by lashing out at the unemployed youth. The article pointed out that youth is too picky and should, contrary to Kong Yiji, take off their gown and accept whatever job is available. The article stated:

“Studying and obtaining academic qualifications can enrich our souls and enhance our abilities. While it [education] allows us to use gain knowledge to be as a stepping stop to see a broader world, [the society should not be] dividing people into three, six, or nine grades and set rules for ourselves and let academic qualifications become a ‘long gown’ that binds hands and feet.”

A similar message was also delivered by the Communist Party Youth League.

This government response sparked more fury; this in turn led to stricter censorship efforts and limits on Kong Yiji-related topics. However, the supportive messages continued, including more in-depth essays. As seen in this externally archived essay, one author negatively assessed this official response:

“This is a structural social problem. But state media, ignoring the elephant in the room, paints it instead as a personal problem: if you cannot find enough jobs, it must be your own fault, and do not blame society.”

In another essay, saved externally, the author argued that:

“We all understand the reason behind [the government’s] asking Kong Yiji to take off his scholar’s gown and go pull a rickshaw. It is a way to solve the problem of a large number of unemployed Kong Yijis by “guiding” them to engage in jobs that have nothing to do with their majors or academic credentials.”

Figure 9: A post on Weibo criticizing the government’s attempts to shift the blame towards youth. It states: “Take off the gown? Are you all joking? I spent more than ten years of painstaking efforts to obtain this gown, but you ask me to take it off? Do you think it is possible? I will not only not be going to take it off, I am going to continue to do my best to improve and enhance my gown.” Source: Weibo post.

Interestingly, the Chinese government has found a relatively easy ‘fix’ to the problem – starting from August, the release of youth unemployment rates will be suspended due to the need to “optimize and improve” statistics. Therefore, while it will be challenging to keep up with the youth unemployment dynamics without access to statistics, one thing is clear: there is no simple remedy to this problem.

Educated youth unemployment is often a recipe for a ticking time bomb; and it is not difficult to find a recent precedent – one of the main reasons behind the Arab Spring was related to unemployed and disillusioned youth. Even if we look at China’s own modern history, the youth that was dissatisfied with the system was one of the main driving forces behind the 1989 Tiananmen Square Protests. Therefore, long-term neglect of this particular social group might evolve into an existential threat for the CCP. However, it is also important to note that the CCP is actively learning from historical precedents, be it the collapse of the Soviet Union, the Tiananmen Square Protests, or the Arab Spring. A relentless censorship system, full control and societal surveillance leaves very little room for the youth to mobilize and form their interest group. The recent crackdown on dissent (notably against the LGBTQ+ community and human rights lawyers) indicates just how tight the system is becoming. While the central government seems to largely ignore the issue at the present time, it will most likely double its efforts to make sure that the CCP remains in control of society at all times.

[1] Financial regulatory guidelines based on three rules: a) liabilities cannot exceed 70% of total assets; b) reserves must be no less than 100% of short-term debt; c) net debt cannot exceed equity by more than 100%.

[2] Upper-class distinction included wearing long gown and drinking while sitting whereas lower-class wore short shirts and drank while standing. Kong Yiji combined both elements as a symbol of his aspirations and harsh reality.

Associate Expert of RESC China Research Program, PhD student at VU Institute of International Relations and Political Science. Raigirdas holds a bachelor’s degree in Asian and Pacific Studies (Chinese Studies) from Lancashire Central University (UK). After studying, he went to China, where he spent five years studying and working. Raigirdas completed a year-long intensive Chinese language and culture course at the Sichuan University (Confucius Institute Scholarship). In 2020, he graduated from Sichuan University (China) with a Master’s degree in International Relations in Chinese. Raigirdas interests: sinology, Chinese foreign and domestic policy, history of the PRC, relations and conflicts between East Asian countries.

Newsletter

Subscribe to regional news and reviews.